Greening the Steel and Cement Used in China’s Global Infrastructure Projects

China’s development finance institutions (DFIs), primarily the China Development Bank (CDB) and the Export–Import Bank of China (CHEXIM), have become central players in global infrastructure development. These DFIs have contributed to economic growth in host countries by unlocking infrastructure bottlenecks, increasing trade and improving infrastructure and energy access. At the same time, China’s overseas infrastructure projects have come under scrutiny for their climate impact.

While attention has often focused on their role in financing fossil fuel versus renewable power projects, this report highlights another critical dimension of climate impact: the massive volumes of steel and cement, both carbon-intensive materials, used in Belt and Road Initiative (BRI) projects. These materials are indispensable for roads, railways, bridges, ports and power plants, yet their production accounts for nearly one-fifth of global CO₂ emissions. The BRI, spanning more than 140 countries, therefore not only shapes energy systems and transport but also locks in material-related emissions for decades.

This report is a joint research effort by Global Efficiency Intelligence and the Boston University Global Development Policy Center. Our report examines the role of green procurement strategies in reducing the carbon footprint of steel and cement used in Chinese-financed infrastructure projects, particularly in the energy and transport sectors.

Steel and cement demand is expected to remain strong in developing economies, especially in Asia and Africa where most BRI projects are located. With Chinese domestic demand for steel and cement plateauing, BRI infrastructure also provides an outlet for China’s industrial production overcapacity in these sectors, which exceeds domestic consumption levels. Against this backdrop, green procurement can be a powerful tool to reduce embodied emissions by embedding low-carbon requirements into the sourcing of cement and steel. In this report, we quantify the material demand and associated emissions in key BRI transport and energy projects, explore green procurement scenarios and discuss implementation pathways that could align Chinese-financed infrastructure with global climate goals.

China’s overseas development finance, representing public and publicly guaranteed loans by CDB and CHEXIM, has provided over US$472 billion in loans since 2008, making it the largest bilateral lender for global infrastructure and development. While this model has expanded economic opportunities abroad, it has also directed vast sums into carbon-intensive sectors. The energy sector is the largest recipient, with $184 billion since 2008, much of it for fossil fuel extraction, coal power and large hydropower. Transport is the second-largest recipient sector, spanning roads, railways, airports and ports, all highly material-intensive.

Steel and cement are at the core of these projects. For example, steel is essential for boilers, turbines and transmission towers that underpin electric power systems, while cement reinforced with rebar forms the foundations of dams, roads and bridges. These materials ensure durability, but they are among the most carbon-intensive to produce. The climate implications are magnified by China’s historic focus on fossil fuels: Chinese-financed power plants around the world already emit 287 million tons (Mt) CO₂ per year, with another 53 Mt likely if planned projects proceed. Lifetime emissions from coal plants with Chinese backing could reach 11 Gt CO₂, about one-third of Asia’s total. Beyond direct emissions, BRI projects often drive deforestation, biodiversity loss and land-use change while also facing climate risks such as floods, typhoons and water stress. This dual dynamic makes it an urgent need to reduce embodied and operational emissions while at the same time improving climate resilience, a central priority for many host countries.

Cement use in energy and transport projects financed by China’s DFIs is estimated to generate 2,452 kt CO₂, assuming all cement is sourced from within the country where the project is located. Completed projects account for the majority, at 1,988 kt CO₂, while projects under construction contribute 406 kt CO₂ and planned projects just 58 kt CO₂. Emissions are highly concentrated, with South Africa, Indonesia, Argentina, Ethiopia and Angola together responsible for about 977 kt CO₂, or 40 percent of the total. This shows that a small number of countries drive a large share of cement-related embodied emissions, and that completed projects dominate the footprint due to the decline in new overseas development finance in recent years.

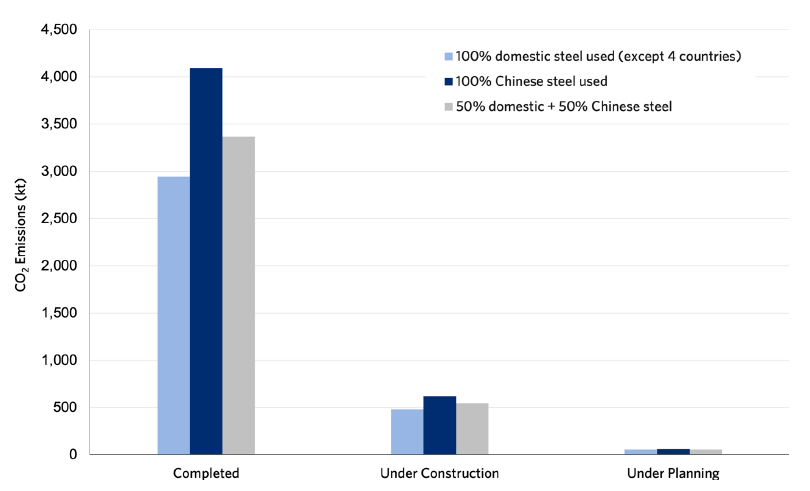

Steel emissions vary more depending on sourcing assumptions. If all steel were produced domestically in BRI partner or host countries (with China supplying only those countries lacking local steel industries), emissions would total about 3,480 kt CO₂, compared with 4,772 kt CO₂ if all steel came from China. We also modeled a scenario with a 50/50 split between domestic and Chinese supply, for which emissions were an estimated 3,966 kt CO₂. In all scenarios, completed projects account for most embodied emissions, with over 2,900 kt CO₂ under the domestic case and more than 4,000 kt CO₂ under the Chinese-supply scenario. The top five countries, Argentina, South Africa, Indonesia, Ethiopia and Angola, make up about 62 percent of steel-related emissions under the domestic case. These results underline that sourcing choices matter: relying on Chinese steel raises emissions by 37 percent due to its higher carbon intensity, while even a mixed approach increases them by 14 percent. Green procurement strategies, therefore, play a crucial role in reducing the carbon footprint of BRI infrastructure projects (see Figure ES1).

Figure ES1: CO2 Emissions Associated with Steel Used in China’s Overseas Development Finance in the Energy and Transportation Sectors

Note: Projects covered in this study include only key transport and energy sectors receiving development finance from China, see Section 3.

For cement, the analysis shows that green procurement could significantly cut emissions from Chinese-financed transport and energy projects. Total cement-related emissions in the dataset amount to about 2,452 kt CO₂, with nearly 2,000 kt CO₂ already locked into completed projects. Applying procurement standards that progressively reduced CO₂ intensity could have delivered meaningful savings: around 351 kt CO₂ in a low-reduction (15%) case, 704 kt CO₂ in a medium case (30%), and over 1,170 kt CO₂ under a high-reduction pathway (50%). The most ambitious scenario, aiming for a 75 percent cut, could have achieved a reduction of 1,758 kt CO₂. While completed projects dominate the footprint, applying such policies to projects under construction and planning would still secure reductions. Beyond direct savings, these policies would create strong market signals for host-country producers to invest in efficiency, clinker substitution and innovative technologies such as Limestone Calcined Clay Cement (LC3), thereby accelerating broader decarbonization.

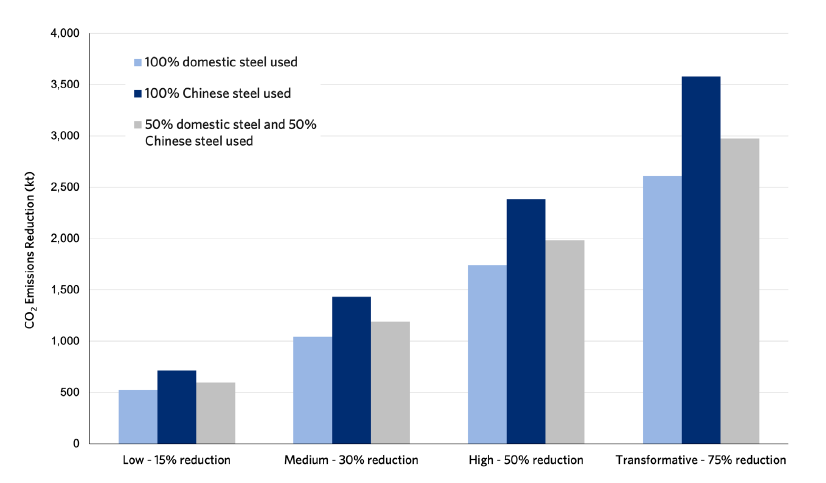

For steel, the emissions reduction potential depends on both the level of procurement ambition and the sourcing mix. Under a low-reduction (15%) target, green procurement could cut 522–716 kt CO₂ depending on sourcing, or about 595 kt CO₂ if steel is split equally between domestic and Chinese supply. These savings grow to 1,044–1,432 kt CO₂ under a medium (30%) target, 1,740–2,386 kt CO₂ under a high (50%) target and 2,610–3,579 kt CO₂ under a transformative (75%) target, with mid-mix projects achieving 1,190, 1,983 and 2,974 kt CO₂ reductions respectively. Most of this potential comes from completed projects, though projects under construction (70–349 kt CO₂) and under planning (8–38 kt CO₂) still add meaningful reductions. The results underline two levers: ambitious procurement targets and smart sourcing. Domestic steel, where electric arc furnace (EAF) routes dominate, generally lowers emissions, while requiring low-carbon standards for imported Chinese steel can drive deeper overall cuts and stimulate decarbonization in both supply regions (see Figure ES2).

Figure ES2: CO2 Emissions Reduction Potential from Steel Used in Analyzed Transport and Energy Projects under Different Sourcing Scenarios

Note: The Chinese development–financed projects covered in this study include only projects in key transport and energy sectors.

The implementation of green procurement for cement and steel in BRI projects faces major challenges. These include gaps in governance frameworks across Chinese and host-country institutions; limited emissions data and reporting capacity; higher costs of low-carbon materials; cost constraints for certain decarbonized steel and cement production technologies; and varying levels of political support for stricter standards. However, strong enablers can support adoption. These include alignment with global green procurement policies; the leverage of Chinese DFIs and state-owned enterprises (SOEs) in driving supply chain shifts; capacity-building for host-country producers; partnerships to scale innovations such as LC3 cement and hydrogen-based steel; and synergies with development goals such as lower energy costs, competitiveness and cleaner air.

Developing a green procurement framework for China’s overseas development finance is essential to reducing the carbon footprint of BRI infrastructure projects. By setting clear standards for low-carbon steel and cement, China can align its global investments with climate goals, support industrial modernization in host countries and maintain competitiveness in increasingly climate-conscious markets. The recommendations summarized in this report highlight actions for ministries, DFIs and SOEs, along with cross-cutting mechanisms to enable effective implementation.

To read the full report and see complete results and analysis of this new study, download the full report from the link above.

Don't forget to follow us on LinkedIn and X to get the latest about our new blog posts, projects, and publications.